As a business owner, you know that your financial statements are not only a reflection of your organization’s financial health. They’re also tools to make better financial decisions to grow your business.

To fully comprehend your company’s financial position, there are three key financial statements you should know about:

- The Balance sheet, which shows your company’s assets, liabilities and net worth on a stated date

- The Income statement, which shows the net income of your company over a stated period

- The Cash flow statement shows the inflow and outflow of cash resulting from your company’s activities in a specified period

To help you understand and make the most of these numbers, here’s a quick crash course on Financial Statements 101.

Related: Income Statements for Small Business Owners

Related: Understanding Financial Statements: A Guide for Small Businesses and Non-Accountants

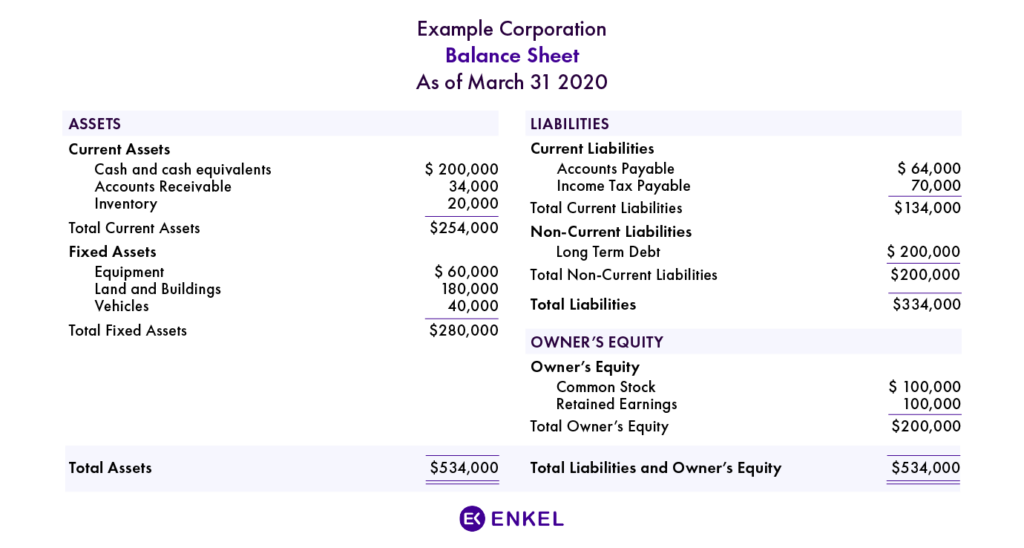

What is a Balance Sheet?

A balance sheet is a snapshot of your company’s finances on a particular date. It provides an overview of your business assets and who owns them: someone else, yourself, or your shareholders.

This is the balance sheet formula:

ASSETS = LIABILITIES + OWNER’S EQUITY

Assets are any items of value and include:

- short-term assets (like accounts receivable or inventory), and

- long-term assets or fixed assets (like office equipment, buildings, or certain investments)

Liabilities are debts and include:

- short-term liabilities (like accounts payable or wages owing), and

- long-term liabilities or long-term debt (like business loans or mortgages)

Owner’s equity, or shareholders’ equity, is the amount belonging to you as a sole proprietor or to your corporation’s stockholders after liabilities have been subtracted from assets.

Balance sheets always show assets on one side and liabilities and equity on the other. The two sides must always balance (hence the name).

By comparing what your company owns to what it owes, the balance sheet keeps you informed about your monetary situation so your business can avoid solvency issues.

The 2026 Nonprofit Financial Checklist

Read More

What is an Income Statement?

Also known as a profit and loss statement, the income statement describes your company’s financial performance in terms of revenue and expense over a specific period. In short, it reports how much revenue your company earned minus the costs and expenses associated with earning that revenue.

This is a typical income statement formula:

PROFIT/LOSS = REVENUE - COSTS

While your gross revenue includes all income generated by your business – including sales of goods and services – your costs are broken out into:

- direct cost of goods sold/cost of sales (how much you paid to produce or provide your product or service), and

- indirect operating expenses (how much you paid for things like rent or advertising)

Gross profit is the result of deducting the cost of sales from gross revenue before deducting operating expenses.

Other line items on your income statement may include:

- customer returns,

- bad debts,

- asset depreciation,

- interest income or interest expense associated with investments or loans, and

- income tax

The final line of the income statement represents your company’s net profit (or loss) - also known as your net income. If you run a corporation, your net income flows into the “retained earnings” that form part of your shareholders’ equity.

Corporate income statements also include a calculation of Earnings per Share (EPS). This number reflects how much money stockholders would receive for each share they own were your business to distribute its net income for the period. Retained earnings, then, are impacted by dividends paid out to shareholders.

Unlike balance sheets, income statements cover a range of time – often three months (quarterly) or one year (annual).

Because they provide a full overview of revenue, expenses, net income, and EPS during that period, examining past data can help you compare trends and better understand how your business has grown.

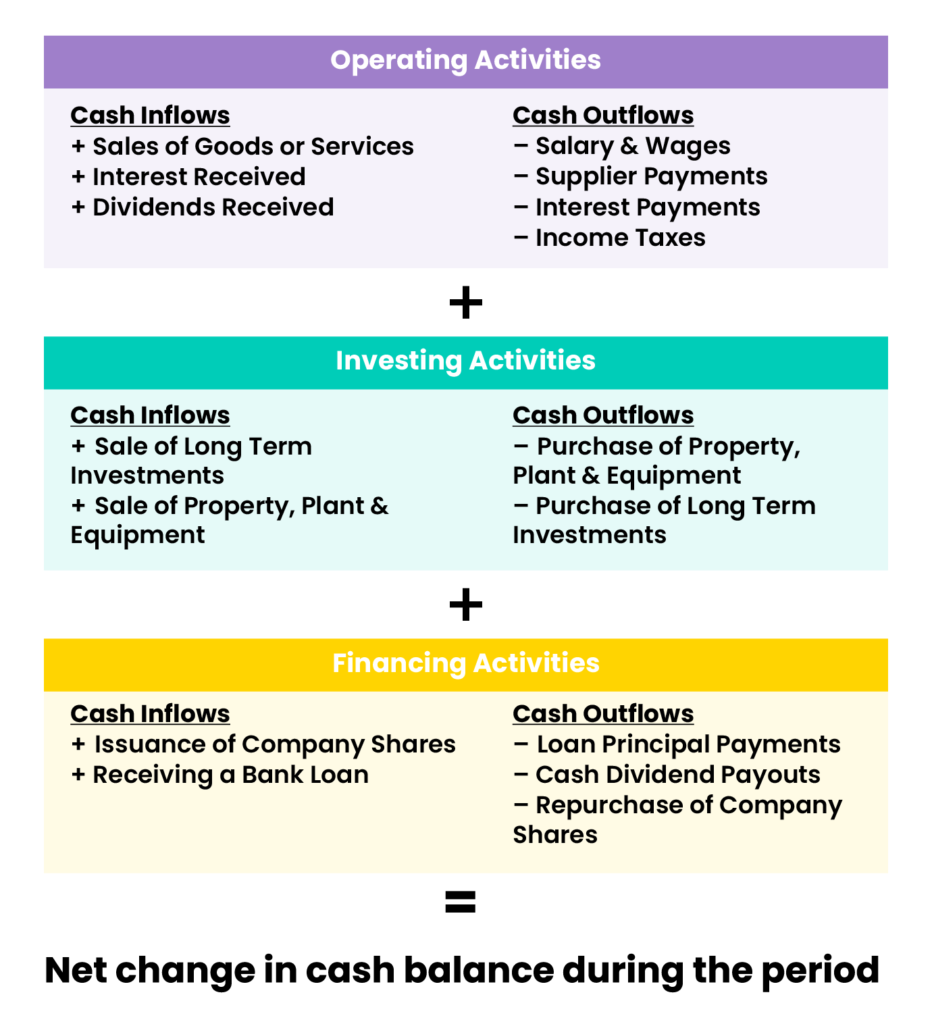

What is a Cash Flow Statement?

A cash flow statement is a detailed and dynamic listing of transactions of the money flowing in and out of your business. The statement of cash flow details where your money is coming from each month (inflowing sources) and where it is going (outflowing sources).

Cash flow statements differ from balance sheets and income statements because they don’t accommodate future cash flow from credit activities.

So, an increase of $5,000 in accounts receivable on your balance sheet over the prior month, for example, would decrease $5,000 in operating cash on your cash flow statement.

Ultimately, a cash flow statement reconciles your income statement with your balance sheet in three major areas: core operations, investing activities, and financing activities.

Cash Flow from Operations

Cash flow from operating activities refers specifically to money moving in and out of your company as a result of your normal business activities.

It provides an overview of how much money flows in as cash collected from sales versus how much is flowing out as payments (to suppliers or employees, for example).

Cash Flow from Investing Activities

When your business experiences changes in its assets, equipment, or investments, these appear in the investing activity section of your cash flow statement.

Most investing activities are considered “cash out.” For example, if you purchase new equipment or renovate a retail space, the money spent will be considered cash outflow.

However, if you’re divesting an asset—by selling a building or excess inventory, for example—the transaction will be considered “cash in.”

Cash Flow from Financing Activities

When your business experiences changes in its debts, loans, or dividends, these appear in the financing activity section of your cash flow statement.

The flow from financing activities is considered “cash in” when capital is raised and “cash out” when the principal on an asset is paid down.

How Can I Use My Financial Statements?

Analyzing the history of your financial statements with a professional bookkeeper will help you better understand where your money is going, allowing you to budget more sensibly.

Reviewing your financial statements regularly will also make it easier to:

- foresee financial problems before they happen,

- spot opportunities for growth and

- secure new financing or investors with a strong income statement and cash flow forecast

While your financial statements tell the story of your company’s past financial performance, the same data can be used to generate projections of how your business will perform.

Because they’re based on historical trends and reasonable assumptions about changes in your business environment, these projections are considered quite credible.

Finally, understanding the numbers on your financial statements is vital for measuring your progress against other companies in your industry. And it is this kind of competitive analysis that can help ensure your business keeps moving forward.

Understanding Different Types of Financial Reports

Why does financial reporting matter?

Financial reporting involves documenting financial activities over a set period. This process helps you stay organized so that, when needed, you can view your organization's financial status.

The report you use will depend on your objective. For example, while you'll want your income statement and balance sheet handy during tax season, an earnings report will be necessary when seeking investments.

As an SMB, financial reporting helps you:

- Maintain detailed records, allowing you to benefit from greater tax savings.

- Understand tax requirements, such as whether you need to charge GST/HST.

- Experience a smoother process if you are audited. Auditors can use other methods to determine income or GST/HST net tax if information is missing.

Balance sheet overview

Your balance sheet is a fundamental document comprising your organization's financial statements.

When analyzing your balance sheet, you'll get a summary of your organization's financial position at a certain time. You can quickly see what you own and owe — understanding the organization's financial health.

The main components include:

- Current assets

- Fixed assets

- Current liabilities

- Long-term liabilities

- Shareholders' equity

Income statement analysis

Income statements, also known as profit and loss statements, are another essential financial document, and your ability to read them is crucial. This statement summarizes all expenses and income over a set period, often shared quarterly or annually.

Like your balance sheet, your income state can help determine your organization's financial health. However, this analysis also lets you set meaningful goals, adjust your business strategy, and predict future opportunities based on financial trends.

Here are the elements of an income statement:

- Revenue

- Expenses

- Cost of goods sold

- Gross profit

- Operating income

- Income before taxes

- Net income

- Earning per share (EPS)

- Depreciation

- Earnings before interest, taxes, depreciation, and amortization (EBITDA)

Following an analysis of an income statement, you can make connections to cut costs and implement growth strategies. For example, you may see that sales are improving or your cost of goods is dropping while the return on equity is rising. You can link this data to current business operations, adapting as needed.

Cash flow statement importance

A cash flow statement showcases profitability, strength, and potential long-term outlook. It provides data on all cash inflows from ongoing operations and external investment sources and shows the amount of cash going out over a specific period.

Use this statement to analyze or share data with investors to indicate where money is going and coming from. Based on this analysis, you'll determine whether your organization has enough cash to meet all obligations and operating expenses.

While these statements are often prepared annually, they can also be created monthly, quarterly, or semi-annually. Cash flow statements report inflows and outflows based on the following activities:

- Operating activities, like taxes, wages, rent, utilities, supplier costs — and cash collected from customers

- Investing activities, like the cost of buying a building or equipment

- Financing activities, like getting a loan, paying a loan, and receiving share proceeds

Read more: The Importance of Cash Flow Statements (And How to Prepare Them)

Interpreting financial ratios

Financial ratios are critical snapshots that help you better understand your organization's financial viability. These ratios can reveal information about your organization, such as whether you've taken on too much debt or are stocking too much inventory.

You can find ratios on financial dashboards and reports to measure performance, broken down into categories such as:

- Liquidity ratios, including current and quick ratios

- Activity ratios are efficiency ratios, including average collection period and inventory turnover

- Profitability ratios, including gross profit margin, return on equity, net profit margin

- Leverage ratios, including debt to equity, debt to assets, and debt coverage ratio

Prioritize your understanding of financial reporting

Whether you want to ensure your budget is on track or make the next tax season a breeze, you must prioritize financial reporting this year and beyond. A comprehensive understanding of different financial reports will ensure more effective

One of the best ways to ensure that your bookkeeping is skillfully executed is to hire a professional. Our team of experts at Enkel is here to help; feel free to contact us. We can assist you with all of your accounting and bookkeeping needs, helping your business grow to new heights.