As one of three key financial statements, your balance sheet (or statement of financial position) says a lot about your business. It shows exactly how healthy your business is at a specific moment in time, including your current debt load and available cash.

For Canadian business owners, understanding your balance sheet is essential. Whether you are applying for a small business loan from a Canadian bank, preparing for year-end tax filing with the CRA, or trying to attract investors, your balance sheet is the first document they will ask to see. Once you understand your numbers, you can easily calculate your organization's net worth and catch cash flow problems before they threaten your operations.

Let's take a deeper dive into what an organization's balance sheet is, how to read it, and how it can benefit your business.

What is a Balance Sheet?

The balance sheet, also known as the statement of financial position, is an overview of:

- what your business/organization owns (assets),

- who owns it (equity), and

- what your business/organization owes (liabilities)

Because these numbers change over time, the balance sheet shows your company’s financial position on a specific date. It also shows your company’s net worth on that date. It does not show results over time. This is what makes it different from your income statement, which tracks net income over weeks, months, or a year.

Subtract your total liabilities from your total assets, and you get your business's net worth. For sole proprietors, that remaining amount is owner's equity. This gives us the basic accounting equation:

This equation always balances, and that's not a coincidence. Every asset your business or organization owns is paid for in two ways. It comes from borrowing (liabilities) or from owners’ funds (equity). If one side changes, the other must change with it.

For clarity, balance sheets often list and total assets on the left side. Liabilities and equity are listed and totalled on the right side. The totals on both sides are always identical.

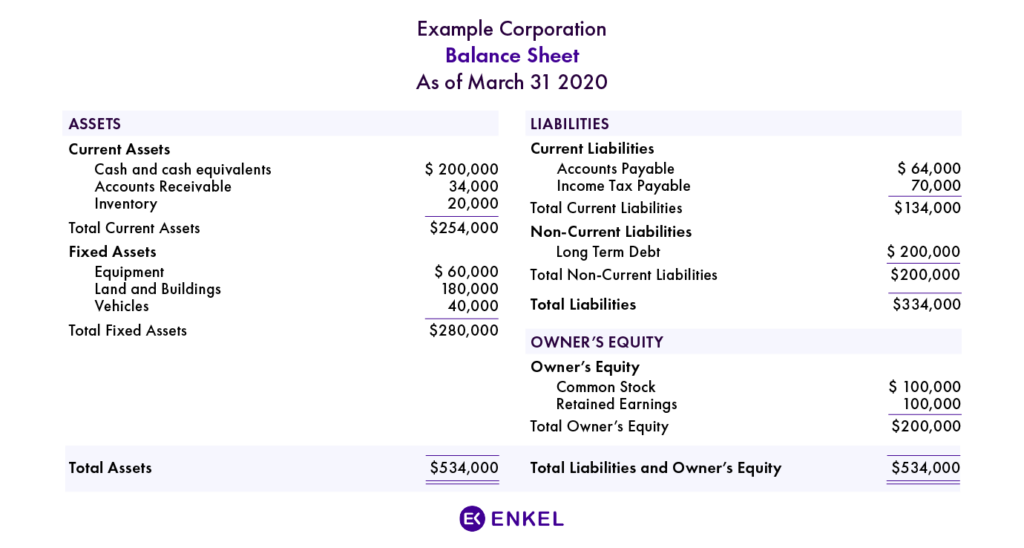

You’ll find a sample balance sheet here:

The 2026 Nonprofit Financial Checklist

Read More

Different ways the Balance Sheet can be used

Your balance sheet serves many purposes, but in each case, it provides a clear understanding of your company's financial standing at a specific point in time.

Who reviews a balance sheet?

People who may have reason to review your balance sheet include:

- Internal stakeholders like yourself, your shareholders, or your management team.

- External stakeholders, such as investors or banks.

- Potential stakeholders include new backers, lenders, or buyers.

As a business owner, you can use the balance sheet to review and manage the relationship between the money inside your company and the money you owe other people.

How can you use it as a business owner?

As a business owner, you can use it to review and manage the link between your company’s money and what you owe others. For example, it can help you figure out whether you can afford to invest in new premises, inventory, equipment, or personnel. It can also help you avoid money problems by showing when it may be time to lower long-term debt. It can also indicate when to convert some assets to cash. When you combine it with net income from your income statement, you and others get a clearer view of your business’s financial health.

How do outside stakeholders use it?

People outside your business may also want to see how your company has performed over time. By applying financial ratios to your monthly, quarterly, and annual statements, lenders, investors, or buyers can assess your business. This includes understanding your credit risk and how much your business can afford to borrow. It also includes your chance of delivering a return on investment. It covers how you compare with others in your industry and your potential for future growth.

By looking for trends and applying financial ratios to your monthly, quarterly, and annual balance sheets, lenders, investors, or potential buyers can determine things like:

- How much of a credit risk does your business represent?

- How much money can you afford to borrow?

- How likely is your business to provide a return on investment?

- How does it compare with other companies in your industry?

- There is significant potential for future growth.

Your balance sheet may be used in different ways. It offers valuable details about your business’s financial stability.

What you'll find on a Balance Sheet

As discussed, there are three types of numbers on a balance sheet: assets, liabilities, and equity. Understanding what fits in each category and how they connect is key to reading your financial statements with confidence.

Assets

Assets are anything your business owns that has value. For better accuracy, accounting systems split a business’s assets into two groups. One group is short-term assets (current assets). The other group is long-term assets (fixed assets).

Current assets include cash and anything that can be converted into cash within one year. Common examples include:

- accounts receivable,

- inventory,

- short-term investments, and

- prepaid expenses like annual insurance premiums

Fixed assets are not easy to convert to cash. They include business equipment, real estate, and intangible assets like goodwill. It’s worth noting that fixed assets depreciate over time. Depreciation expense reduces your net income on the income statement. This can affect retained earnings on your balance sheet. This is one of the clearest examples of how your financial statements are connected.

Liabilities

Liabilities are debts your business owes. Similar to assets, they are divided into short-term liabilities (current liabilities) and long-term liabilities (non-current liabilities).

Current liabilities include amounts due within one year. Common examples include:

- accounts payable,

- taxes or dividends owing,

- short-term loans, and

- wages, salaries, or other amounts owing to employees

Non-current liabilities are debts due after one year. They include bonds you issued and long-term loans. Examples are leases, mortgages, and loans for vehicles or equipment. Keeping an eye on your liabilities-to-equity ratio helps you understand your business’s financial health. This ratio is also called the debt-to-equity ratio. It also shows how much risk your business is carrying.

Equity

The amount left over after deducting everything your business owes from everything it owns is called equity. If you're a sole proprietor, this belongs to:

- If you own a business as a sole proprietor, your assets minus liabilities belong to you. This is called owner’s equity.

- If your business is a corporation, the difference between assets and liabilities belongs to stockholders. This is called stockholders’ equity, or shareholders’ equity.

Equity also includes capital that you or other owners invest in the business. It also includes retained earnings, which are profits the business reinvests over time. Retained earnings grow when net income is strong and reinvested instead of paid out. A healthy equity section often shows strong long-term financial health.

Reviewing your financial statements

When reviewed alongside your income statement and cash flow statement, the balance sheet is very helpful. It is essential for understanding where your business has been and where it is going.

How do the three statements work together?

Think of it this way. Your income statement shows your net income over a set period. The cash flow statement then shows how money moves in and out of the business. Tying it all together, the balance sheet shows the cumulative result of all financial decisions up to that date. None of these three statements tells the full story on its own. But together, they give a complete and honest view of your business's financial health.

How often should you review them?

Review them often, monthly if you can, and at least quarterly — so nothing catches you off guard. Spotting trends early becomes much easier when you check in regularly. Knowing if your equity is growing or shrinking helps you stay prepared. Having the numbers ready for a lender, investor, or buyer puts you in a stronger position.

About Enkel

Working through financial numbers isn't for everyone, and that's completely okay. The good news is that with the right support and clear guidance, those reports don't have to feel overwhelming. When you have someone to help break things down, making sense of your financial statements becomes far easier and much more manageable.

Enkel provides the visibility you need to understand where your business stands and where it's headed. Contact us today to learn more.

Frequently Asked Questions (FAQ)

Here are answers to common questions business owners ask about balance sheets. Learn how to read one. See how it connects to your other financial statements.

What is a balance sheet used for?

A balance sheet shows your business’s financial position at a specific time. It lists what you own (assets), what you owe (liabilities), and the difference (equity). Business owners use it to assess net worth, support loan applications, and monitor overall financial health. Investors and lenders use it to evaluate credit risk and potential return on investment.

What is the basic balance sheet formula?

What is the basic balance sheet formula?

The foundational accounting equation is: Assets = Liabilities + Equity. This equation always balances. Every asset your business owns is funded by debt (liabilities). Or it is funded by the owners' investment and retained earnings (equity). The two sides of a balance sheet must always be equal.

What is the difference between current and non-current assets?

Your business can convert current assets into cash within one year; examples include cash, accounts receivable, inventory, and prepaid expenses. Non-current (fixed) assets take more than a year to convert, such as real estate, equipment, and intangible assets like goodwill. This distinction matters when assessing your business's short-term liquidity.

How does net income affect the balance sheet?

Net income from your income statement flows directly into the equity section of your balance sheet as retained earnings. When your business earns a profit and reinvests it, retained earnings grow, which increases total equity. This is why you should review net income with your balance sheet. It gives a clearer view of your business’s financial health over time.

How often should a business prepare a balance sheet?

Most businesses prepare a balance sheet monthly, quarterly, and annually. Monthly statements help you spot trends early and manage cash flow. Quarterly statements are often required for lenders or investors. Annual statements are essential for tax filing and long-term financial planning. The more frequently you review it, the earlier you can address potential financial health issues.

What is the difference between a balance sheet and an income statement?

A balance sheet is a snapshot of your business finances on a specific date. It shows assets, liabilities, and equity. An income statement covers a period of time and shows revenue, expenses, and net income. Together, they tell a complete story: the income statement shows how you performed, while the balance sheet shows where you stand.

What is owner's equity on a balance sheet?

Owner's equity, also called shareholders' equity in corporations, is the business's net worth. It is what remains after you subtract total liabilities from total assets. It includes capital you or other owners have invested, plus retained earnings accumulated over time. Growing equity is generally a sign of strong financial health, as it means the business is building value.

Can a balance sheet show if a business is in financial trouble?

Yes. Warning signs include liabilities higher than assets (negative equity). They also include current liabilities much higher than current assets (poor liquidity). Another warning sign is declining retained earnings over time. Lenders and investors use financial ratios on balance sheet data, such as the debt-to-equity ratio. They use these ratios to assess credit risk and overall financial health before making decisions.