Quick Summary

We look at the basics of cash flow statements for small businesses and not-for-profit organizations. We explain why cash flow statements are important for your business’s financial health and how to prepare them. Cash flow statements provide valuable insights into a company's financial health by detailing the movement of cash through operating, investing, and financing activities. This information is crucial for identifying potential financial risks and making informed financial decisions.

The 2026 Nonprofit Financial Checklist

Read More

Why is it important to understand cash flow?

Although cash flow is considered one of the most important measures of long-term business strength and profitability, a study commissioned by QuickBooks found that:

- 64% of Canadian small businesses have experienced cash flow issues

- 25% estimate they have more than $20,000 in outstanding receivables

- 33% of businesses with cash flow problems have been unable to meet certain payment obligations

Understanding the data on your cash flow statement is essential for defending your business against improper cash management. While having cash on hand is important, it’s your cash flow that signals whether or not your business can generate cash consistently and use it efficiently.

A business with good superficial financial performance can still fail due to poor cash flow management. Think of your cash flow statement as a real-time snapshot of your financial flow. It reveals where your cash comes from (sales, investments), where it goes (expenses, debt payments), and ultimately, if you will have enough on hand to cover upcoming bills and opportunities. A cash flow statement helps you predict potential shortfalls, adjust spending accordingly, and secure financing. In short, a well-managed cash flow keeps your business breathing, while neglecting it can lead to suffocation, even with good profitability.

No matter how much income your company generates on paper, for example, you’ll have trouble achieving sustainable, positive cash flow if you regularly spend more than you’re bringing in to:

- Pay employees

- Purchase supplies and meet overhead costs

- Float business loans, lines of credit, or credit card expenses

Most cash flow problems are the result of not being able to pay debts when they’re due. That said, it’s not uncommon for small businesses to owe more than they earn from time to time.

You may experience a temporary cash-flow shortfall, for example, when you:

- Invest in large quantities of inventory

- Purchase essential but expensive equipment

- Hire new staff to keep up with operational demand

However, consistently poor cash flow management is one of the leading causes of small business failure.

Fortunately, using cash flow statements to track the movement of money in and out of your business can help prevent many problems before they occur. If you're looking to generate projections, a cash flow forecast will help you identify where (and when) you may run out of cash.

What is a cash flow statement?

A cash flow statement is a financial report that shows the total amount of money flowing in and out of your business over a specific period. By delineating where your money is coming from and going to, cash flow statements demonstrate:

- Your company’s liquidity or working capital in the form of available cash

- Cash-related changes in company assets, liabilities, or equity

- Hard numbers that can be used to forecast future cash flow

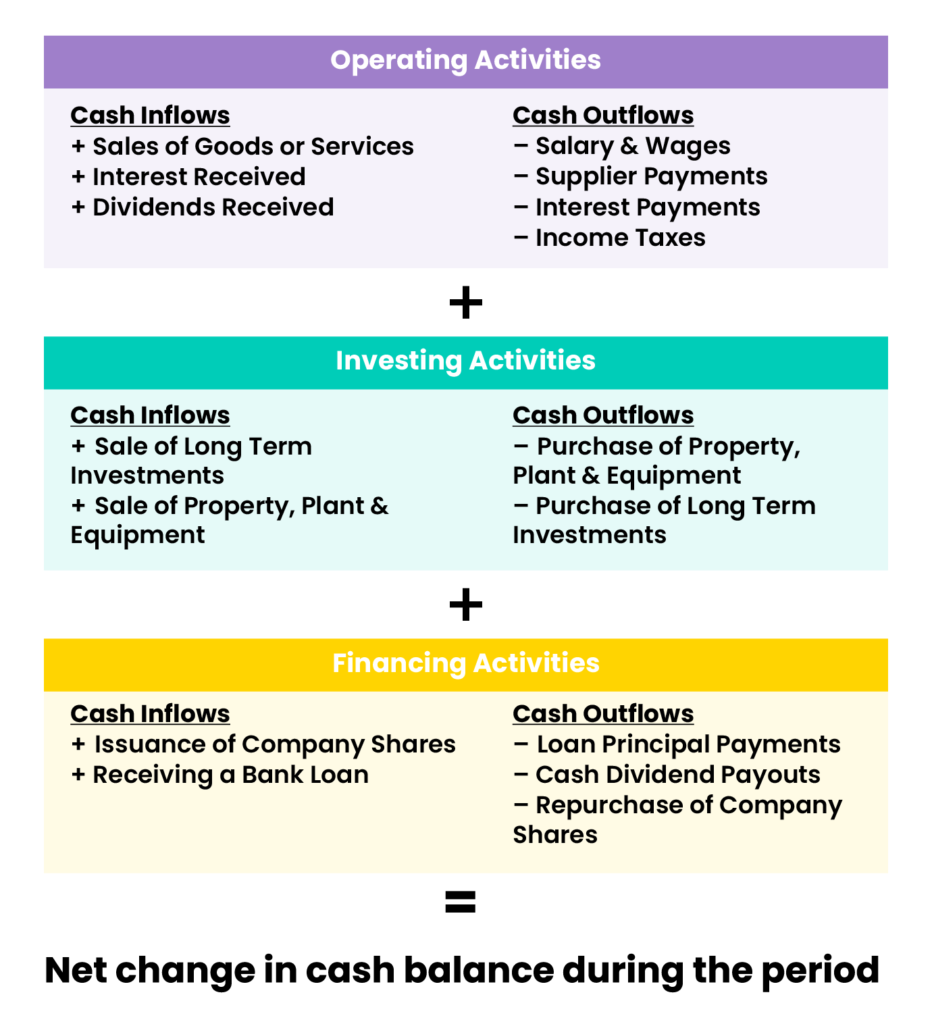

Along with your balance sheets and income statements, cash flow statements are critical to proper account management. A cash flow statement effectively reconciles the figures on your income statement with what’s on your balance sheet by adding up business activity in 3 key areas: operations, investment, and financing.

Structure of a Cash Flow Statement

When interpreting the data in a cash flow statement, it’s important to understand the individual components. They include:

- Cash flow from operating activities

- Cash flow from investing activities

- Cash flow from financing activities

Operating Activities + Investing Activities + Financing Activities = Cash Available from the Accounting Period

Based on this formula, cash flow statements make monitoring cash inflows and outflows easy and compare period-over-period cash balance changes.

Let’s look closer at the three sections of the cash flow statement.

Operating activities

Cash flows from operating activities show the movement of cash in and out of your company as the result of normal business activities. This would include the money you collect from sales or pay out to suppliers and staff.

Investing activities

Flow from investing activities shows cash changes involving company assets or other investments. Examples of outflow activities include purchasing a commercial space or equipment, while incoming cash flow from investments would include selling off assets like inventory or real estate.

Financing activities

Cash flow from financing activities shows money movement related to debts, loans, or dividends. Incoming cash flows from financing are driven by activities that raise capital (like selling company shares, for example), while outflows include things like paying down your loan principal.

How to calculate a cash flow statement

There are two ways to prepare a cash flow statement.

With the direct method, you record every instance of cash entering or leaving your business as it happens and use those cash transaction amounts to generate your monthly cash flow statement.

If, for example, your cash balance at the end of the previous month was $5000 - and you recorded gross cash receipts of $3,000 and gross cash payments of $1000 this month - your cash flow statement for the period would show cash on hand of $7,000 ($5,000 + $3,000 - $1,000).

With the indirect method, you work backwards from your net income to calculate cash flow and your ending cash balance for the period.

If, for example, your income statement showed a net income of $3,000, you would adjust that amount to reflect depreciation and amortization and to incorporate cash events from operating, investing, and financing activities.

Direct methods:

- Are more straightforward

- Leave a clear paper trail

- Suit small businesses with few income sources and non-cash assets

Most businesses, however, use indirect methods because they’re less work to track and provide a level of financial detail that goes beyond simple cash flow from operations.

Either way, using cloud accounting software like QuickBooks Online or Xero makes it easy to pull relevant account data and generate cash flow statements.

How to Interpret Your Cash Flow Statement

Preparing cash flow statements allows you to perform valuable cash flow analyses, but only if you can successfully interpret the information in them. Analyzing your statements can make it easier to pre-empt cash flow issues and help you plan around growth opportunities. Knowing how to interpret the information in your cash flow statement is key because it's an important step to understanding the financial health of your business and proactively addressing any cash flow issues.

Key areas you should consider when reviewing your cash flow statement include:

- Net cash flow from operating activities. This number might not be positive every month, but the overall trend should be toward growth, year-over-year. If yours isn't, there are likely some operational issues you need to address.

- Outstanding accounts receivable. The more money you have tied up in uncollected customer payments, the less cash is available to your business for managing debt and expenses. Seeing a large or growing number here is a sign that you are not managing the accounts receivable function effectively.

- Investments and capital expenditures. Costly or unplanned expenses can have a large and lengthy impact on cash flow.

Many cash flow problems arise from a mismatch between when money enters your business and when it leaves. This could be the result of overestimating your ability to collect payments from customers while also managing expenses.

You may be able to fix timing issues by:

- Stretching out supplier payments to the full term

- Optimizing your collections schedule

- Preparing for equipment upgrades or obsolescence

- Focusing on your accounts receivable function and nudging customers to pay their bills on time

Regular analysis won’t just help you understand your company’s current cash situation. You can also use cash flow data to generate projections around how your business will perform in the future.

Cash Flow Statement vs. Income Statement vs. Balance Sheet

We know the world is mostly made up of non-accountants and the information contained in the various types of financial statements can be confusing to interpret and then translate into actionable outcomes. Here is a brief overview of the different types of financial statements, their purpose, and how to use the information you find in them.

| Financial Statement | Purpose |

| Cash flow statement | Gives insights into the company’s financial health by tracking the inflow and outflow of cash |

| Income statement | Also known as a profit and loss (P&L) statement, the income statement reports on revenues, expenses, gains and losses experienced in a particular period of time |

| Balance sheet | Gives clarity to what the company owns (assets) and owes (liabilities) as well as shareholder equity. |

If working with numbers isn’t your forte, Enkel can manage your day-to-day bookkeeping and help you create the cash flow statements you need to budget more sensibly. Find out how our accounting services help keep businesses strong over the long term.

How to Improve Cash Flow

Increase your cash flow by going paperless

In recent years, there’s been a trend with businesses and non-profits moving to a completely paperless ecosystem. Apart from being environmentally friendly, removing the need for physical paper administration can save precious time and money. A paperless cash flow ecosystem increases efficiency and cost-effectiveness by reducing the time and resources spent on manual data entry and physical storage of paperwork. Bookkeeping software automates many bookkeeping tasks, such as categorizing transactions and generating reports, which reduces errors and frees up time. Reducing paper usage and storage needs also lowers ongoing material and office space costs, contributing to a more sustainable business practice.

Going paperless with electronic invoices

Using cloud-based online accounting software, like QuickBooks Online or Xero, allows businesses to create and send online invoices directly to clients via email. The online invoice will also contain a “Pay now” link to make it easy for clients to settle the invoice. The easier you make it for clients to pay you, the faster you are likely to receive payment.

Both Xero and QuickBooks Online enable automated invoicing for recurring invoices, as well as gentle follow-up reminders for outstanding invoices.

Going paperless with online payments

You can also go paperless by accepting credit cards or online payments instead of using cheques.

It can take several business days for a cheque to clear because it has to move between the various parties (from your customer to you, from you to your bank, and then from your bank back to your customer’s bank to request payment). Cheques are also more expensive due to the handling fee associated with them.

Domestic online payments, on the other hand, will take one business day to clear (sometimes instant, depending on the payment method) and have a lower processing fee associated with it.

Automate your billing process

Many small businesses know they should improve their cash flow. But with so many aspects in the cash flow ecosystem that can impact the cash flow cycle, it can be difficult to know what to tackle first.

To start with, there are two simple optimizations with your receivables you can address today that are sure to have an almost immediate positive impact on your cash flow:

- Sending out your invoices on time

- Making it easy for your clients to pay you

Send out your invoices on time

It sounds simple enough, but with time being a rare commodity in any small business, billing often gets delayed. The sooner you send out invoices, the sooner the payment terms will kick in, the quicker you will receive payment, the healthier your cash flow will be.

Make it easy for your clients to pay you

If your clients have to move from one platform to the next, manually entering details into their bank, double-checking that the amount is correct, and manually logging it into their accounting software, your invoice is likely to be set aside until they have at least half an hour of free time to complete the whole process.

As previously mentioned, your online accounting software can be used to send electronic invoices with links that take your clients directly to the payment options. If customers can pay an invoice within five minutes of opening their email, chances are your invoice will be settled much quicker.

Both of these aspects can be addressed through automated billing. Manual processes are prone to human error, which can take time to fix, delaying payment even further.

An example of an automated billing platform is Plooto.

Plooto can be integrated with your accounting software to automatically import unpaid invoices and bills. It makes it easy for clients to pay through email, credit card, or pre-authorized debits. It can also be programmed to send automatic, gentle payment reminders.

Improving cash flow is not just about accounts receivable. You should also monitor your accounts payable and look for suppliers offering discounts on early payments.

Software such as Beanworks can automate payments on the accounts payable side, allowing you to take full advantage of maximum vendor payment terms while still making sure you pay suppliers on time to avoid late payment fees or interest.

Create a cash flow forecast

Cash flow forecasting allows businesses to take a proactive, rather than reactive, stance toward their current cash position. This will give you time to respond to any identified potential future cash shortfalls.

Software like Dryrun allows cash flow data from QuickBooks Online or Xero to be imported and then adjusted so businesses can test different scenarios based on when cash is expected to come in and when bills are due.

Instead of just paying vendor invoices when they come in (which is rarely a good strategy) and running the risk of depleting cash reserves, business owners can strategize and plan when to pay certain bills without ruining the relationship with a supplier.

It also gives you time to plan how to use expected future cash surpluses to grow the business overall.

There is arguably a better feeling for any small business owner than seeing a positive cash flow at the end of the month, and nothing reduces stress levels more than knowing your cash flow is under control and being managed effectively. With these cloud technology tools in your arsenal, you can focus on improving other areas of your business without having to worry about your cash flow.

At Enkel, we help small business owners automate their billing process through cloud-based technology and our professional team of accountants and bookkeepers. Whether your company is located in Vancouver, Edmonton, Calgary, or Toronto, we've got your bookkeeping needs covered! Contact us today to learn more.